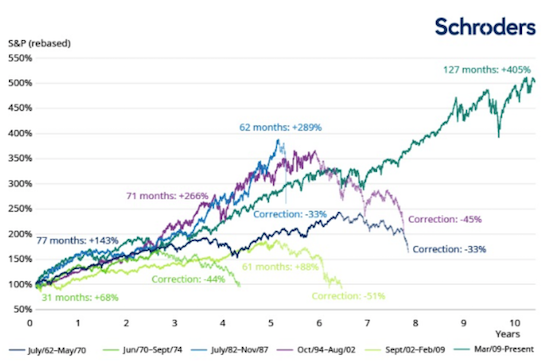

Six biggest bull markets in US stocks/shares since 1962 and their subsequent bear markets.

The chart below shows the six biggest bull markets in US stocks/shares since 1962 and their subsequent bear markets.

In this example a bull market is defined as a rise of 50% or more over a period lasting more than six months. A bear market is defined as a fall of 20% or more that lasted at least three months.

The six biggest bull runs since 1962 (and their corrections):

Summary of Market Corrections since 1929

1929: The Worst Stock Market Crash in History

· Dow loss: 89%

· Time to recover: 25 years

1973: The Oil Crisis and Economic Recession

· Market loss: 48%

· Time to recover: 21 months

1987: Asset Price Bubble and Stock Market Panic Selling

· Market loss: 33%

· Time to recover: 24 months

2000: The Dotcom Bubble

· Nasdaq loss: 77%

· Time to recover: 15 years

2008: The GFC and Subprime Mortgage Crisis

· S&P 500 loss: 57%

· Time to recover: 17 months

2020: The COVID-19 Crash

· Market loss: 34%

· Time to recover: 33 days

Let’s put the current market correction into perspective

If you have been invested in the Australian or US stock markets for more than 10 years, your

personal or super portfolio is still well ahead in terms of performance over the long-term.

Stock market performance since 1997:

Source: https://tradingeconomics.com/australia/stock-market

- Blue = ASX200 (Australian shares)

- Orange = S&P500 (U.S. shares)

- Green = NASDAQ (U.S. Technology shares)

Current falls since the last peak (as 30/09/2022):

Source: https://tradingeconomics.com/australia/stock-market

- ASX200 (blue line): -15.1% (peaked at 7,620 points on 5/01/2022)

- S&P500 (orange line): -25.2% (peaked at 4,796 points on 3/01/2022)

- NASDAQ: (green line) -34.1% (peaked at 16,057 points on 19/11/2022)

We have been through market falls in the past and each time the market recovers to new highs. The only question is how long this current one will take.

The current fall in stock markets may also provide an opportunity to add to existing portfolios or sectors of the market at a discount to the previous two years. However, you need to be prepared for the potential of further falls before the recovery begins.

What Investors Can Do Now

Crashes and downturns are part of investing—and the only way to lose money during a market dip is if you sell your investments. If history is any indication, your investments will make up their losses in time.

Still, in moments of volatility and uncertainty, there are things you can do to shore up your finances.

Pay off high interest debt

Any debt higher than 8% is known as toxic debt. That’s because the stock market traditionally returns an annual rate of 8 to 9%, so any debt higher than that is debt that loses you money. Credit cards and high-interest personal loans often fall into this category. To manage toxic debt, make a budget and a payoff plan. This will help you take control of your money and build your credit. It will also put you in a good position to start an emergency fund, if you haven’t already.

Have an emergency fund

Experts agree that everyone should have an emergency fund, or a liquid cash safety net, in case something happens like losing your job or another financial burden. Usually 3 to 6 months of expenses is preferred, although some experts argue that upwards of 9 months to a year of expenses is best. The best place to keep an emergency fund is in a high-yield savings account.

Don’t spend excessive amounts of money

Times of economic uncertainty may not be the moment to buy that new TV or car. In case of a recession, it’s best to keep your money where you can see it: in a fully funded emergency fund and if you can, invested.

Make sure your investments are diversified

Once you make sure your ducks are in a row—aka your high interest debt is paid off and your emergency fund is fully funded—investing is a great next step. Many investors find opportunities like this to invest, as stocks are “on sale.”

Investing is for everyone, regardless of age. And the sooner you start investing, the better.

Diversifying your investments and spreading out your money among hundreds of different companies is what experts agree you should do to build a robust investment portfolio. However, investing in individual stocks/companies takes specific skills and a lot of time to research. For the average person, choosing a reputable fund manager is an easier and less risky way of investing. Index funds are a great option too. These funds track a market index or a particular sector of the market.

Invest Regularly

It is impossible to time the markets – we never know when the market reaches the top or the bottom of its cycle until well after the event has occurred. There is no magical bell that rings to tell us – we only really know in hindsight. So the best approach is to keep investing regularly.

Keep “dollar-cost averaging”, or putting the same amount of money into your investment or super accounts every month, to keep a steady stream of money going into your accounts in order to grow your wealth. Even if the markets keep falling for a while, you will be adding to your portfolio at ever cheaper prices which will over time appreciate in value.

The best way to cope when the market starts to go down is to stick to your plan, remember why you’re investing, and follow your regular investment schedule.